Tokenization is just a dumpsite for private credit

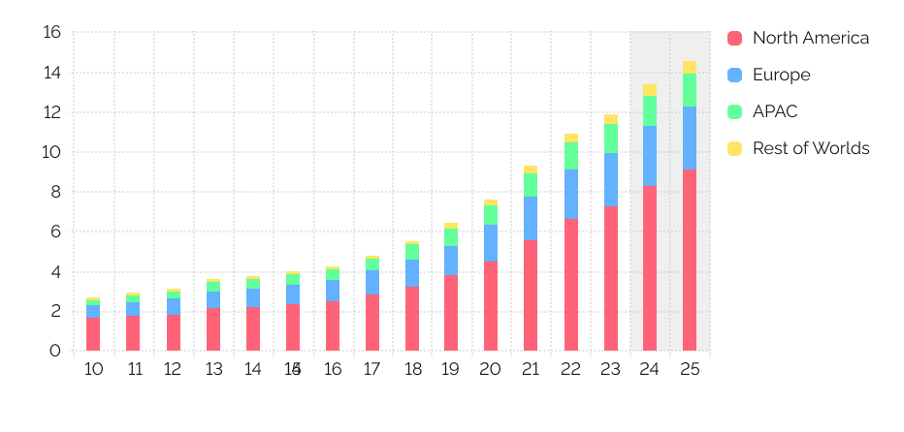

Private Markets which until recently were perceived as a niche for a small circle of specialized managers, have evolved over the past decade into a huge and, apparently, systemically important segment of our financial system. As of 2024, the total assets under management in private markets exceeded $14 trillion, comparable to the GDP of the world's largest economies. Since 2014, the industry has grown by an average of 14% per year, with the most rapid acceleration occurring during periods of excess liquidity, particularly after the pandemic. Moreover, approximately two-thirds of all capital is concentrated in North America, highlighting not only the geographic concentration but also the dependence of the entire structure on the dollar-denominated financial system. However, the key issue lies in the changing structure of the industry. While classic private equity used to be the core of private markets, today we are dealing with a much more complex system. The industry's largest players have transformed into financial conglomerates. Blackstone manages assets of $1.1 trillion, KKR over $550 billion, and Carlyle over $440 billion. In terms of scale and functions, they have long since gone beyond the scope of classic funds and have transformed into an alternative banking system.

Growth in assets under management in the private markets sector, $ trillion

Source: Preqin, Rosenberg Research

This growth has been a direct consequence of two processes triggered by the 2008 crisis. Basel III reforms tightened capital, liquidity, and leverage requirements for high-risk assets, including leveraged buyouts, commercial real estate, and junk bonds. Basel IV continued this trend, limiting internal risk models and sharply increasing the regulatory costs of private market transactions. Banks began to scale back their activities in the riskiest segments, and private equity funds stepped into the emerging vacuum. At the same time, central banks kept rates near zero for over a decade, and institutional managers, from insurance companies to university trusts, began systematically seeking additional returns in a world where traditional asset classes had ceased to generate them. For example, in one of its most recent reports, 71% of the Harvard University Trust's portfolio was allocate to alternative investments segment, a proportion quite typical for such large trusts nowadays.

Asset Allocation in Harvard University's Portfolio, %

Source: top1000funds.com

The combination of these factors explains the explosive growth of the private credit market. By 2023, this segment reached approximately $1.6 trillion, having grown nearly sixfold in a decade. The financial system, previously defined by bank balance sheets, has become increasingly defined by the balance sheets of asset managers. The mechanics of the system appear simple at first glance. A fund raises capital, uses it to finance transactions, creates debt instruments, which are then structured, securitized, and redistributed among investors. Banks do not disappear, but their role changes, as they provide credit lines and infrastructure but do not carry risk on their balance sheets. Thus, a parallel credit system has emerged. Private credit offered financing faster than banks, with fewer requirements and greater risk tolerance. It filled niches ranging from mid-market lending to restructurings. But it is important to understand that this growth was the result of risk redistribution, not risk reduction. Essentially, we have achieved classic financial arbitrage. From the regulators' perspective, the risks seemed to have decreased, as they were removed from banks' balance sheets. From investors' perspective, stable returns were achieved. But in reality, the risk simply shifted to a less transparent part of the system.

The fundamental fragility of this structure lies in the fact that it operates as long as its expansion last. Unlike the banking system, which is itself a source of money creation, private credit requires a continuous influx of new funds to maintain profitability, fund issuance, and initiate new transactions. When this influx ceases, the system has no internal mechanism for maintaining equilibrium. This dependence on constant growth is exacerbated by the fact that asset valuations in private lending are determined not by the market, but by the lenders' own internal models, which are revalued quarterly and in current conditions inevitably overstate the actual market value. Furthermore, most transactions are structured through complex chains of SPVs. The level of real leverage is often impossible to accurately determine. The same assets can be pledged multiple times. Investors see the return, but they don't see the risk structure. Renovo provided a vivid illustration of this hidden risk in November 2025, when the company's debt was nominally valued at 100 cents on the dollar a month before it filed for bankruptcy, wiping out $150 million in creditors' money.

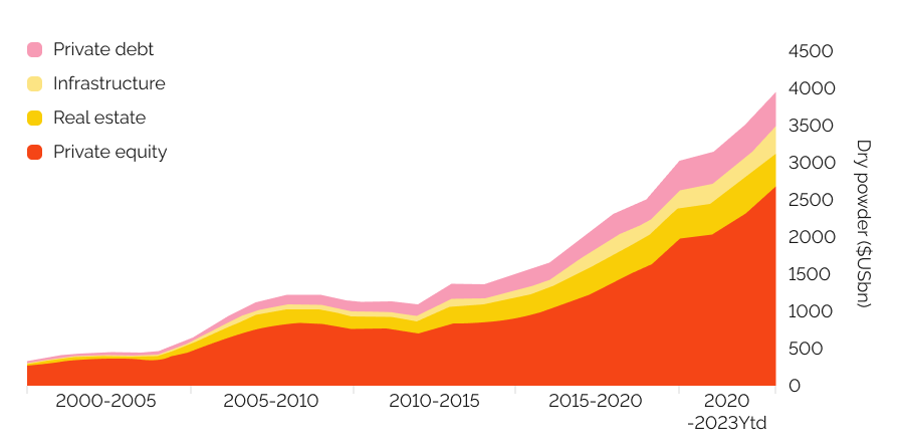

Since 2022, when central banks began sharply raising rates, the segment has entered a turbulent zone. Deals built on cheap debt have become economically unattractive. Borrowers are faced with rising debt servicing costs. Refinancing has become more difficult, and the flow of new deals has begun to decline. According to Fitch, the default rate in the private credit segment has reached approximately 7.8%. Meanwhile, approximately 40% of borrowers have negative cash flow. Their ability to service debt has halved over the past three years. At the same time, another imbalance is accumulating, as the volume of uninvested capital in private markets has exceeded $4 trillion. In a normal phase of the cycle, this would be considered growth potential, but today’s availability shows the funds cannot be deployed effectively.

Uninvested capital in the private markets sector, $ billion

Source: FT

The First Brands case last year became the first major signal of how fragile the entire structure was. A company with a real business and stable cash flows found itself embedded in a multi-tiered financing system. As interest rates rose, the refinancing model faltered. The value of debt instruments fell by approximately 85%. Meanwhile, the total amount of liabilities remained unclear for a long time, with estimates ranging from $10 billion to $50 billion, which in itself speaks to the level of opacity in the system. If even a relatively large and visible company can't accurately assess its debt levels, what's happening in less transparent market segments?

Estimates of the scale of the problem currently diverge, and can essentially be boiled down to two camps. The first believes that the stress in private lending remains localized and poses no systemic threat. The second sees the situation as a manifestation of a deeper vulnerability accumulated over a decade of cheap money. The arguments in favor of a more conservative case appear compelling at first glance. The banking system is indeed in a more secure position than in 2008. Banks' exposure to private credit is relatively limited and typically structured through senior loans. Moody's estimates that the total volume of such exposure is approximately $300 billion, the vast majority of which is secured tranches. Against the backdrop of the trillions of dollars in banking system balance sheets, this appears a manageable risk. Banks themselves also emphasize their resilience, and at first glance, the figures support this. Citi estimates its exposure at about $22 billion, JPMorgan about $50 billion, with more than 95 percent of those positions being senior loans.

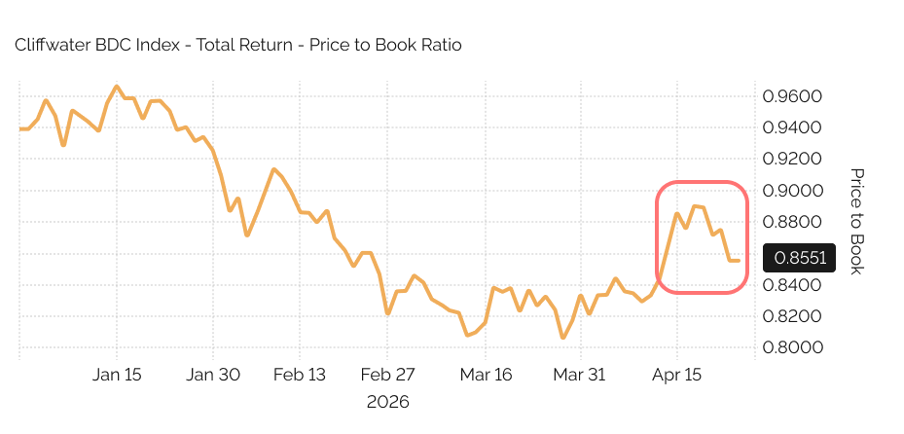

But this argument misses a key point, as the potential private credit problem does not need to manifest itself through the banking system to become systemic. Unlike the 2008 crisis, where risks were concentrated on bank balance sheets, today they are distributed across the entire ecosystem of institutional investors. Pension funds, insurance companies, trusts, family offices, and publicly traded funds are the ultimate holders of these risks. And they determine the system's resilience, something the market is already beginning to factor in. Discounts on private lending funds to net asset value (NAV) are widening. The use of so-called payment-in-kind mechanisms, whereby the borrower increases the principal amount of the debt instead of making a cash interest payment, is growing, a classic sign of a late stage in the credit cycle. Prices of publicly traded instruments linked to private markets are declining, reflecting worsening expectations regarding asset quality and the ability to refinance them.

Stress in private lending

Source: Bloomberg

Since the private markets industry cannot remain stable without a new influx of capital, we are currently witnessing an attempt to access new levels of liquidity in two directions. The first is the so-called democratization of private markets through pension savings. Access to private equity and private credit instruments through 401k individual retirement accounts, the primary retirement savings vehicle in the US, gives the industry access to trillions of dollars in long-term capital. This is an ideal investor from a structural perspective, as it does not require liquidity, is not sensitive to short-term volatility, and is prepared to invest for decades to come. The second direction is related to tokenization, which at first glance appears to solve one of the key problems of opacity, as the transfer of assets to the blockchain allows for the verification of collateral in real time, tracking the structure of liabilities, and reducing information asymmetry.

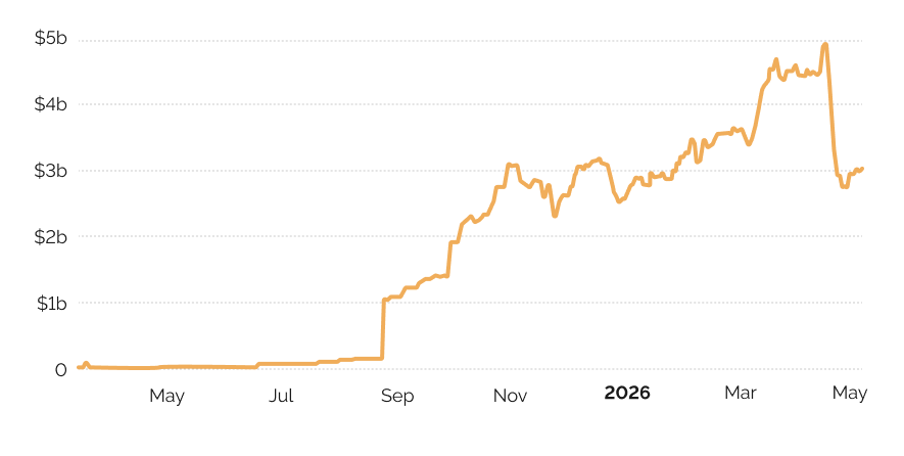

The tokenization infrastructure is already in place, and its scale is growing rapidly. The volume of tokenized private loans grew from $49 million in April 2025 to $3 billion by May 2026. The market has split into two fundamentally different segments. The first segment, which accounts for 93 percent of the market, is structured so that any participant can contribute capital directly to a lending pool, without intermediaries and entry barriers. Maple SyrupUSDC, integrated into the Morpho, Pendle, Aave, and Kamino lending protocols, has become the leader in this segment. This segment has experienced explosive growth, as the lack of entry barriers has attracted capital from retail cryptocurrency market participants seeking returns above deposit rates. The second segment, which accounts for only 6.8 percent, is structured differently and replicates the logic of traditional funds, with investor due diligence, a closed structure, and professional management, only wrapped in tokens.

As the market professionalizes, this segment will become the driver of tokenization growth. However, the speed of further tokenization evolution largely depends on the position of regulators, primarily the SEC and FCA, as the adoption of clear rules for tokenized securities could dramatically accelerate the influx of institutional capital, while protracted regulatory uncertainty will keep major players stuck in the pilot stage.

Market capitalization of tokenized Private Credit, $ billion

Source: RWA.xyz

From a technological perspective, tokenization is truly a step forward. It increases transparency, speeds up settlements, and reduces operational complexity. However, it does not change the nature of the underlying asset. If the loan quality is weak, tokenization does not improve its quality; it merely simplifies its distribution. Moreover, tokenization increases the risks in such a scenario by adding liquidity where none existed previously, creating the illusion of a potentially quick exit from an illiquid asset. In a stressful situation, this can lead to sharp price movements that do not reflect the fundamental value, but merely a reaction to an attempt to exit the position. A classic gap arises between the liquidity of the instrument and the illiquidity of the underlying asset. Furthermore, the legal aspect remains unresolved. Owning a token does not always imply a direct claim on the collateral in the event of default. Issues of claim priority, enforcement of rights, and jurisdiction remain open. In a real-world stress situation, it is the legal structure, not the technological framework, that will determine the investor's ultimate outcome.

Given the challenging situation in private markets, we must assume that tokenization will now be used as a channel for transferring illiquid and toxic assets to a wider audience, including retail investors and pension funds. We are essentially repeating the dynamics of 2007–2008, when securitization performed the same function, redistributing risk across the system until liquidity disappeared. Today, the key difference is scale. The leverage level is significantly higher, the dependence on refinancing is greater, and therefore the potential consequences are more systemic. Tokenization in this context becomes a digital version of the same logic, but with a faster rate of adoption.

Yes, tokenization will certainly remain and will eventually become part of the financial system, as it increases the transparency and efficiency of the infrastructure. However, at this stage, it is primarily a tool for extending the credit cycle and redistributing risk. Its full maturation will require time, including the resolution of legal and structural restrictions. Therefore, in the near future, it is precisely this segment that will carry increased risk, which investors must consider when building their portfolio.